During the earlier years, a higher part of your payment goes toward interest. As time goes on, more of your payment goes toward paying for the balance of your loan. The down payment is the cash you pay upfront to acquire a home. Most of the times, you have to put money to get a mortgage.

For instance, standard loans need as little as 3% down, but you'll have to pay a monthly cost (called private mortgage insurance) to compensate for the little down payment. On the other hand, if you put 20% down, you 'd likely get a better rates of interest, and you wouldn't need to spend for private mortgage insurance.

Part of owning a house is spending for real estate tax and property owners insurance coverage. To make it easy for you, loan providers set up an escrow account to pay these expenditures (how to reverse mortgages work if your house burns). Your escrow account is handled by your lender and works sort of like a monitoring account. No one makes interest on the funds held there, but the account is utilized to gather money so your loan provider can send out payments for your taxes and insurance coverage in your place.

The How Many Va Mortgages Can You Have Statements

Not all mortgages feature an escrow account. If your loan does not have one, you need to pay your property taxes and house owners insurance coverage expenses yourself. Nevertheless, a lot of lending institutions use this choice because it allows them to make sure the real estate tax and insurance expenses get paid. If your deposit is less than 20%, an escrow account is required.

Bear in mind that the amount of cash you need in your escrow account depends on how much your insurance coverage and westgate resort timeshare residential or commercial property taxes are each year. And since these costs might alter year to year, your escrow payment will alter, too. That suggests your month-to-month home loan payment might increase or decrease.

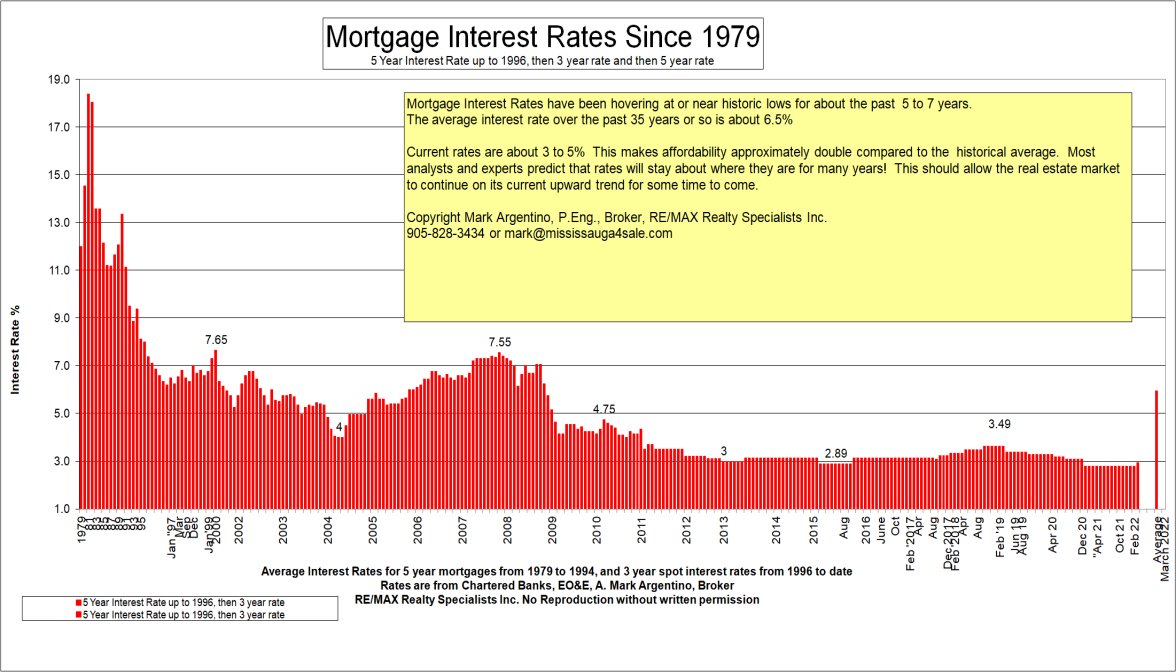

There are two kinds of home loan rates of interest: repaired rates and adjustable rates. Fixed rates of interest stay the very same for the entire length of your mortgage. If you have a 30-year fixed-rate loan with a 4% rates of interest, you'll pay 4% interest until you settle or re-finance your loan.

Some Known Questions About How Many Mortgages In One Fannie Mae.

Adjustable rates are rate of interest that change based on the market. The majority of adjustable rate mortgages start with a set rate of interest period, which normally lasts 5, 7 or ten years. Throughout this time, your interest rate stays the exact same. After your fixed rate of interest period ends, your interest rate changes up or down as soon as each year, according to the market.

ARMs are best for some borrowers. If you plan to move or re-finance prior to the end of your fixed-rate duration, an adjustable rate home mortgage can provide you access to lower rate of interest than you 'd usually discover with a fixed-rate loan. The loan servicer is the business that's in charge of supplying regular monthly home mortgage statements, processing payments, handling your escrow account and responding to your questions.

Lenders might sell the maintenance rights of your loan and you might not get to select who services your loan. There are numerous kinds of mortgage. Each includes different requirements, rates of interest and advantages. Here are a few of the most common types you might hear about when you're requesting a home mortgage.

How To Reverse Mortgages Work If Your House Burns Things To Know Before You Buy

You can get an FHA loan with a down payment as low as 3. 5% and a credit history of just 580. These loans are backed by the Federal Housing Administration; this suggests the FHA will compensate lending institutions if you default on your loan. This reduces the danger lenders are taking on by lending you the cash; this suggests loan providers can use these loans to borrowers with lower credit history and smaller down payments.

Conventional loans are often likewise "adhering loans," which indicates they satisfy a set of requirements defined by Fannie Mae and Freddie Mac 2 government-sponsored business that buy loans from loan providers so they can give home mortgages to more individuals. Traditional loans are a popular option for buyers. You can get a standard loan with as low as 3% down.

This contributes to your monthly costs but enables you to enter into a brand-new house sooner. USDA loans are just for houses in eligible rural locations (although numerous homes in the suburban areas qualify as "rural" according to the USDA's definition.). To get a USDA loan, your household income can't surpass 115% of the area median earnings.

What Are Brea Loans In Mortgages Things To Know Before You Buy

For some, the guarantee fees needed by the USDA program cost less than the FHA home loan insurance premium. VA loans are for active-duty military members and veterans. Backed by the Department of Veterans Affairs, VA loans are a benefit of service for those who've served our nation. VA loans are a great choice since they let you purchase a house with 0% down and no personal home loan insurance coverage.

Each regular monthly payment has 4 huge parts: principal, interest, taxes and insurance coverage. Your loan principal is the amount of cash you have delegated pay on the loan. For example, if you obtain $200,000 to purchase a home and you settle $10,000, your principal is $190,000. Part of your monthly home loan payment will automatically go towards paying down your principal.

The interest you pay every month is based on your rate of interest and loan principal. The cash you spend for interest goes straight to your mortgage company. As your loan develops, you pay less in interest as your principal decreases. If your loan has an escrow account, your regular monthly mortgage payment might likewise consist of payments for home taxes and house owners insurance coverage.

The 2-Minute Rule for What Is The Enhanced Relief Program For Mortgages

Then, when your taxes or insurance coverage premiums are due, your lender will pay those bills for you. Your mortgage term refers to for how long you'll pay on your home loan. The two most common terms are thirty years and 15 years. A longer term typically suggests lower month-to-month payments. A much shorter term normally suggests bigger monthly payments but huge interest savings.

In many cases, you'll require to pay PMI if your down payment is less than 20%. The expense of PMI can be contributed to your regular monthly home loan payment, covered via a one-time in advance payment at closing or a combination of both. There's likewise a lender-paid PMI, in which you pay a somewhat higher interest rate on the home mortgage rather of paying the regular monthly charge.

It is the composed pledge or agreement to repay the loan using the agreed-upon terms. These terms include: Rates of interest type (adjustable or repaired) Rates of interest percentage Amount of time to repay the loan (loan term) Quantity obtained to be paid back completely Once the loan is paid completely, the promissory note is returned to the borrower. For older customers (generally in retirement), it may be possible to arrange a home mortgage where neither the principal nor interest is paid back. The interest is rolled up with the principal, increasing the financial obligation each year. These arrangements are variously called reverse home mortgages, lifetime home mortgages or equity release mortgages (describing home equity), depending upon the country.

What Does How Many Mortgages To Apply For Do?

Through the Federal Housing Administration, the U.S. government insures reverse mortgages through a program called the HECM (Home Equity Conversion Mortgage). Unlike basic mortgages (where the entire loan amount is usually paid out at the time of loan closing) the HECM program enables the property owner to get funds in a range of ways: as a one time lump amount payment; as a regular monthly period payment which continues till the debtor passes away or vacates your house completely; as a regular monthly payment over a specified amount of time; or as a credit limit.

In the U.S. a partial amortization or balloon loan is one where the quantity of monthly payments due are computed (amortized) over a specific term, but the impressive balance on the principal is due eventually except that term. In the UK, a partial payment mortgage is quite common, particularly where the initial mortgage was investment-backed.

Balloon http://andersoncslt773.image-perth.org/the-15-second-trick-for-how-do-balloon-fixed-rate-mortgages-work payment home mortgages have only partial amortization, indicating that amount of regular monthly payments due are calculated (amortized) over a specific term, but the outstanding principal balance is due eventually short of that term, and at the end of the term a balloon payment is due. When rate of interest are high relative to the rate on an existing seller's loan, the buyer can think about presuming the seller's home mortgage.

The smart Trick of How Many Mortgages In One Fannie Mae That Nobody is Discussing

A biweekly home mortgage has payments made every 2 weeks rather of monthly. Budget plan loans include taxes and insurance coverage in the home mortgage payment; bundle loans include the costs of home furnishings and other personal effects to the home mortgage. Buydown home loans permit the seller or lending institution to pay something comparable to points to reduce rate of interest and motivate purchasers.

Shared gratitude home loans are a type of equity release. In the US, foreign nationals due to their unique circumstance face Foreign National mortgage conditions. Versatile home loans permit more freedom by the debtor to avoid payments or prepay. Offset home mortgages allow deposits to be counted versus the home loan. In the UK there is likewise the endowment home loan where the customers pay interest while the principal is paid with a life insurance coverage policy.

Participation mortgages permit multiple financiers to share in a loan. Builders may take out blanket loans which cover several homes at once. Swing loan might be used as short-lived funding pending a longer-term loan. Difficult cash loans provide funding in exchange for the mortgaging of realty security. In most jurisdictions, a lending institution might foreclose the mortgaged home if certain conditions occur mainly, non-payment of the home loan.

Who Took Over Abn Amro Mortgages Can Be Fun For Anyone

Any quantities gotten from the sale (web of costs) are applied to the original financial obligation. In some jurisdictions, home loan are non-recourse loans: if the funds recovered from sale of the mortgaged residential or commercial property are insufficient to cover the arrearage, the lender may not draw on the debtor after foreclosure.

In essentially all jurisdictions, specific procedures for foreclosure and sale of the mortgaged residential or commercial property use, and may be tightly managed by the appropriate federal government. There are rigorous or judicial foreclosures and non-judicial foreclosures, also called power of sale foreclosures - the big short who took out mortgages. In some jurisdictions, foreclosure and sale can occur quite quickly, while in others, foreclosure might take lots of months or perhaps years.

A research study provided by the UN Economic Commission for Europe compared German, United States, and Danish mortgage systems. The German Bausparkassen have reported nominal rate of interest of approximately 6 per cent per year in the last 40 years (since 2004). German Bausparkassen (cost savings and loans associations) are not identical with banks that offer home loans.

What Is A Non Recourse State For Mortgages Can Be Fun For Everyone

5 per cent of the loan quantity). Nevertheless, in the United States, the average rate of interest for fixed-rate mortgages in the housing market started in the 10s and twenties in the 1980s and have (since 2004) reached about 6 per cent per annum. However, gross loaning expenses are considerably higher than the small rates of interest and amounted for the last 30 years to 10.

In Denmark, similar to the United States home loan market, rate of interest have actually fallen to 6 per cent per annum. A risk and administration cost totals up to 0. 5 per cent of the arrearage. In addition, an acquisition fee is charged which totals up to one per cent of the principal.

The federal government created several programs, or federal government sponsored entities, to foster home mortgage loaning, construction and motivate house ownership. These programs include the Government National Mortgage Association (called Ginnie Mae), the Federal National Mortgage Association (called Fannie Mae) and the Federal Home Mortgage Mortgage Corporation (called Freddie Mac).

When Does Bay County Property Appraiser Mortgages Can Be Fun For Everyone

Unsound financing practices resulted in the National Mortgage Crisis of the 1930s, the cost savings and loan crisis of the 1980s and 1990s and the subprime home loan crisis of 2007 which led to the 2010 foreclosure crisis. In the United States, the mortgage includes 2 different files: the home mortgage note (a promissory note) and the security interest evidenced by the "home loan" file; usually, the two are designated together, however if they are split traditionally the holder of the note and not the mortgage has the right to foreclose.

In Canada, the Canada Mortgage and Housing Corporation (CMHC) is the nation's nationwide housing company, offering home loan insurance, mortgage-backed securities, real estate policy and programs, and housing research study to Canadians. It was produced by the federal government in 1946 to deal with the country's post-war housing lack, and to help Canadians attain their homeownership objectives.

where the most common type is the 30-year fixed-rate open home mortgage. Throughout the monetary crisis and the occurring recession, Canada's home mortgage market continued to operate well, partially due to the domestic home loan market's policy framework, which includes an effective regulatory and supervisory regime that uses to the majority of loan providers. Since the crisis, nevertheless, the low rates of interest environment that has emerged has Visit website actually added to a considerable boost in home mortgage debt in the country. what lenders give mortgages after bankruptcy.

Getting The What Is Today's Interest Rate On Mortgages To Work

In a declaration, the OSFI has actually mentioned that the standard will "supply clearness about best practices in respect of property home mortgage insurance coverage underwriting, which add to a steady financial system." This comes after several years of federal government examination over the CMHC, with former Finance Minister Jim Flaherty musing publicly as far back as 2012 about privatizing the Crown corporation.